The global M&A slump – can the slump present investment opportunities?

William Abell

by William Abell

The recent slump in global M&A activity has been widely reported, with Reuters claiming that global dealmaking in Q1 2023 fell to its lowest level in over a decade. Bloomberg reports that Q1 and Q2 of 2023 held the second- and third-lowest quarterly deal volumes since 2017; only Q2 2020, when we were in the throes of the Covid-19 pandemic, was worse.

WTW data reveals that deal activity in transactions of over USD 100 million slowed significantly around the world during the first half of 2023, with a total of 280 deals completed compared to 441 during the same period in 2022. This represents a 37% drop in volume and the lowest figure for the first half of a year since 2009. It certainly feels like a long way from the record-breaking deal activity of 2021.

The reasons for the slump in activity are well documented. The rise in interest rates across the globe has resulted in the end of cheap credit. The increased cost of debt has naturally curbed M&A activity. Increased borrowing costs have been felt particularly hard by the private equity sector where leverage is at the core of the business model. The first quarter of 2023 marked the fifth in an unprecedented string of consecutive quarterly pullbacks in private equity investment. According to Bloomberg data, no other drop in the aggregate volume of PE-backed deals has ever run longer than three quarters. This comes despite the huge amounts of unspent capital that many private equity funds continue to sit on in the wake of the Covid-19 pandemic.

The other significant factor impacting M&A activity is global geopolitical turmoil, including Russia’s war with Ukraine and the deteriorating relationship between China and the US, amongst other factors. Such turmoil undoubtedly increases uncertainty and reluctance amongst buyers to proceed with transactions.

As Michael Aiello, chairman of the corporate department of law firm Weil, Gotshal & Manges LLP, remarked recently, “Global uncertainty is what is impacting M&A most – it just makes people uncomfortable. It's easier to say, I'll pass on a deal – nobody gets fired for passing on a deal. But we all talk about the deal that never should have happened.”

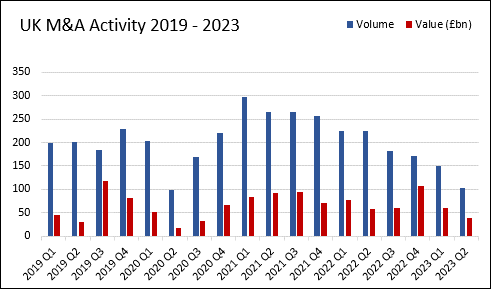

The UK M&A trend mirrors global trends, where transaction volumes have steadily declined since 2021.

Data: M&A of UK Companies where transaction size exceeded GBP 1millionSource: Pitchbook, collated by Gerald Edelman LLP

Whilst there has undoubtedly been a slowdown in M&A activity, can the slump present opportunities?

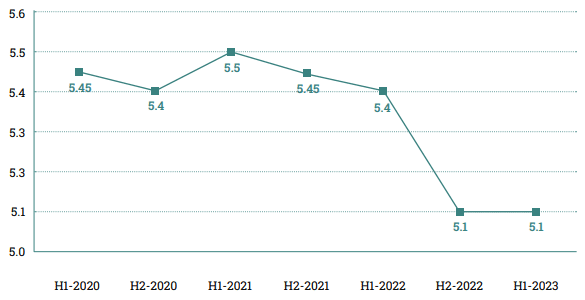

UK multiples are down

The average EBITDA multiple paid in UK M&A transactions has fallen from a peak of 5.5x in 2021 to 5.1x in the past 12 months.

Data: Average EBITDA multiple paid in UK M&A ‘mid-market’ transactionsSource: Dealsuite

Reduced M&A activity has inevitably resulted in lower valuations, presenting an opportunity for potential buyers with the financing in place to move swiftly.

Distressed sales

The United Kingdom is also grappling with economic turmoil as businesses face financial difficulties amidst high inflation, increased energy costs, and a decrease in consumer confidence resulting from the ongoing cost-of-living crisis. The aftermath of Covid-19 has left many companies burdened with substantial debt, leading to a surge in insolvencies. Total UK insolvencies in 2022 were 57% higher than 2021 and H1 2023 numbers continue to indicate another tough year for the corporate sector as business insolvencies trend 16% higher than in H1 2022.

This crisis is significantly impacting certain sectors more than others. Sectors such as construction, manufacturing, and hospitality, among others, are particularly impacted. An October 2022 report indicated that 35% of hospitality businesses expressed concerns about potential collapse by year-end. The situation is unlikely to improved significantly by then given that inflation, interest rates, and cost of living pressures remain heightened, further dampening consumer sentiment.

In the construction sector, rising energy and raw material costs, unpaid bills, labour shortages, supply chain disruptions, and inflation have created a "perfect storm" for businesses, with financial experts at Red Flag Alert warning of over 6,000 insolvencies across the sector in 2023, and 32,000 insolvencies across all sectors.

Against this backdrop, there are ample opportunities for financially robust buyers to acquire distressed companies at low valuations. They can choose to wait for economic stability to return or invest to help struggling businesses achieve immediate growth. For instance, a wave of insolvencies could reduce the pool of construction companies vying for contracts, potentially offering significant opportunities for businesses in the sector that have managed to survive the recent turbulence.

Distressed M&A is not limited to the UK alone, as concerns about recession, rising prices, supply chain disruptions, and inflation are affecting businesses worldwide, especially in Europe, the region most impacted by Russia's ongoing conflict in Ukraine. In a recent survey by CMS, 20% of European dealmakers expressed their motivation to pursue acquisitions in the coming year due to the opportunities arising from high levels of business distress.

Low valuations and financial distress are likely to continue driving substantially distressed M&A in the current year. However, another significant factor impacting inbound M&A in the UK in 2023 is the weakness of the British pound.

GBP weakness

The UK pound took a battering during 2022 – at one point falling to an all-time low of 1.03 against the US dollar. While the end of Liz Truss’ disastrous tenure as Prime Minister gave sterling a lift, the depressed GBP currency valuation still puts UK-based buyers at a disadvantage to overseas parties who have already begun pouncing on distressed businesses and assets amid the ongoing economic upheaval.

What is the outlook?

According to PricewaterhouseCoopers'recent Global M&A Industry Trends 2023 mid-year update report, a significant number of dealmakers in the UK are biding their time, waiting for the right opportunity as valuations decrease and capital begins to circulate once more.

"But that's not to say that the market will look the same as before," the Industry Trends report said. “This is no doubt a challenging market, but we remain optimistic that the coming months will see new opportunities for those that have prepared well. The days of riding valuation multiples are over – and that means putting value creation at the heart of every deal.”

William Abell is a Director with Gerald Edelman. Most of his work focuses on transactions, such as undertaking buy-side financial due diligence in connection with a corporate acquisition, negotiating and advising on a sales purchase agreement on the sell-side, and everything in between. Other areas of practice include forensic accounting and expert witness support, preparing financial models and valuations and, more recently, technical IFRS accounting support (including the preparation of UK listed IFRS accounts), which builds on his previous Big 4 experience. Contact William.

XLNC member firm Gerald EdelmanLondon, England, UKT: +44 20 7299 1400

Audit, Accounting, Tax, Corporate Finance, Strategy, Management Consulting