Real estate investment into Germany as a foreign individual / foreign corporation

Andreas Lang

by Andreas Lang

Germany offers a stable and attractive environment for real estate investment, with its strong economy, transparent legal system, and robust property market.

However, foreign investors need to be aware of the tax and other regulations governing real estate transactions to optimize their investments and avoid risks.

This article provides an overview of the key tax considerations, including property acquisition tax, ongoing taxation of rental income, and tax on property disposals.

Understanding these regulations is essential for ensuring compliance and maximizing returns in the German real estate market.

1) Considerations when purchasing real estate in Germany

In general, real estate in Germany may be purchased and owned by German and foreign individuals as well as German and foreign entities.

In order to purchase a property, the purchase contract needs to be concluded before a notary.

Once the purchase price is paid and the respective property transfer tax, land register fees as well as the notary fees are paid, the title of the property is transferred to the new owner.

Real Estate transfer tax (RETT):

Generally, any transfer of German property triggers the German real estate transfer tax. This is true for a direct transfer of the asset as well as in case of a share deal of an entity owning real estate. Further, there are several exemptions with respect to the property transfer tax.

The rate of the German real estate transfer tax varies between the different states and ranges from 3.5 % to 6.5 % of the property value.

Other transaction costs:

It is important to note, that besides the real estate transfer tax there are other significant transaction costs, when purchasing real estate in Germany:

Notary fees: Approx. 1 % - 1.5 % of the purchase price

Realtor fees: Depending on the nature and location of property the rates can very 3 % - 8 % of the purchase price

Land register fees: Approx. 0.5 % of the purchase price

Property tax:

When owning real estate in Germany, an annual property tax is due, which is applied on the assessed value of the property. The assessment follows a different approach in the different provinces.

In order to determine the property tax, the assessed value is multiplied by 0.0035 as well as a multiplier specified by the municipality the property is located in. Therefore, the property tax rate will be different, depending on the specific location of the property.

2) Taxation of rental income from real estate in Germany

Based on the German income tax act, any income derived from renting of real estate located in Germany is taxable in Germany. Therefore, a foreign individual (who is neither resident nor domiciled in Germany) owning real estate in Germany is subject to limited tax liability in Germany and has to file a respective income tax return.

Since most of the double taxation treaties concluded by Germany with other jurisdictions provide for the taxation of real estate income in the country where the real estate is located, no double taxation should result in this respect.

The income tax rates for individuals in Germany (depending on the income) can reach up to 45%. While German tax residents can deduct a basis personal allowance amount, an individual with only limited tax liability in Germany can not deduct this amount and the full profit (after deduction of respective expenses) will be taxed in Germany.

As a corporation with rental income from real estate located in Germany, the above regulations of the double taxation treaties apply accordingly. Therefore, the respective income is taxable in Germany.

In general, a corporation in Germany is subject to corporate income tax as well as trade tax. While the corporate income tax rate is 15 % throughout Germany, the rate of the trade tax varies between the different municipalities (the average is approx. 14 %). However, if the foreign corporation does not constitute a permanent establishment in Germany from a tax perspective, no trade tax is applied on the rental income derived and this income is therefore only subject to German corporate income tax of 15 %.

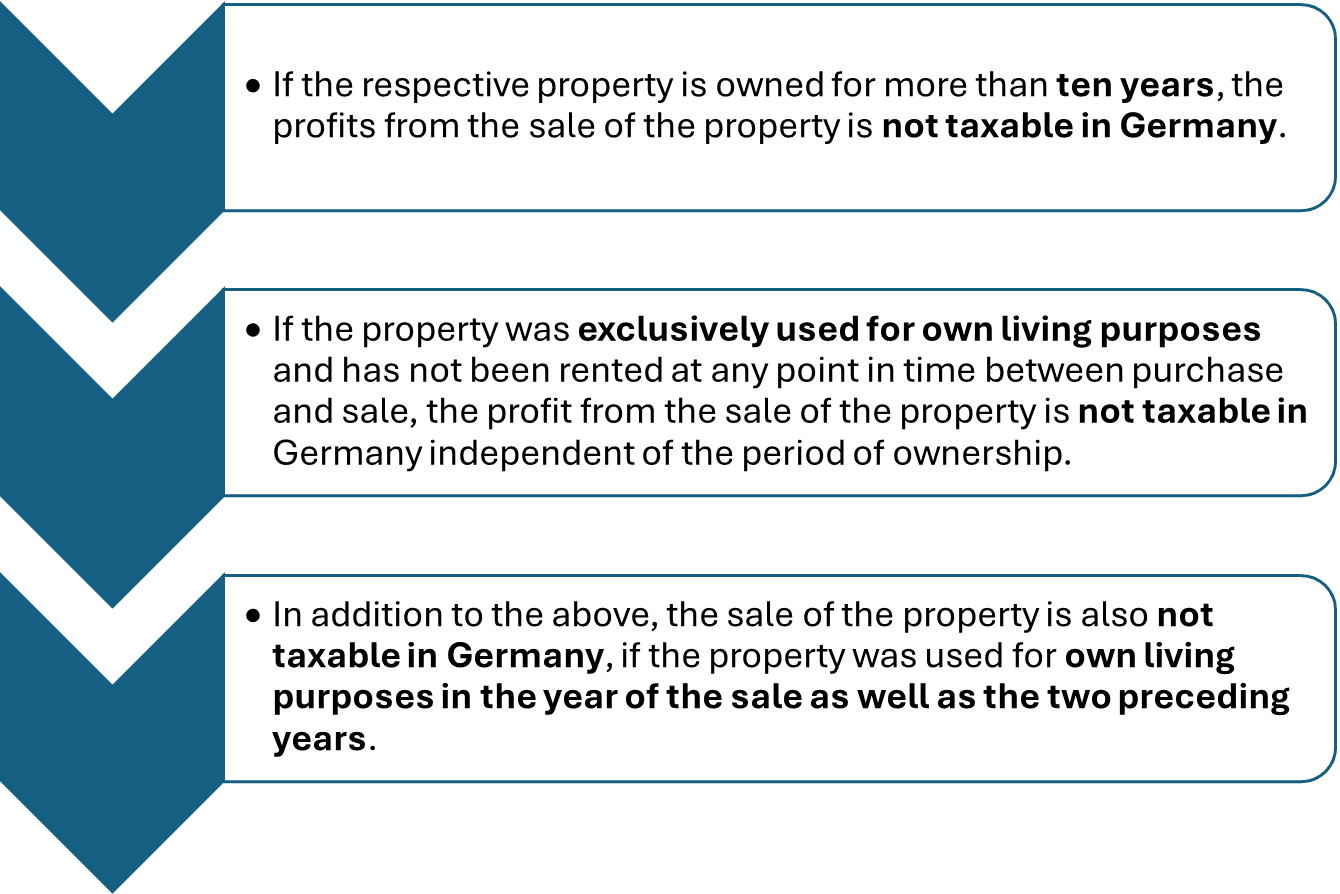

3) Selling real estate in Germany

With respect to selling of real estate in Germany, the general remarks above apply with respect to the taxability of the respect income in Germany.

However, it is important to note that under certain circumstances, real estate located in Germany and sold by an individual can be sold tax free:

If real estate in Germany is owned by a (foreign) corporation, the arising income from the property is generally table in in Germany.

If real estate is held by a business, the sale of the property is generally taxable in Germany. If a real estate property is privately held there are certain exclusions that can result in a tax-free capital gain from the sale of the property. This generally also applies for foreign owners that are not considered a tax resident in Germany.

4) Other consideration resulting from owning real estate in Germany

Inheritance and gift tax:

If real estate owned by an individual who is not a tax resident of Germany is gifted to or inherited by an individual who is also not a tax resident of Germany, the transfer might still be subject to German inheritance / gift tax.

Schlecht und Partner bundles different specialisations and forms a powerful team in complex consulting assignments. They advise entrepreneurs, companies and individuals in all business and tax matters and conduct audits for medium-sized companies. Based on their broad technical and industry expertise, they have a vast experience in SME consulting.

XLNC member firm Schlecht und PartnerStuttgart, GermanyT: +49 711 40 05 40 30Auditing & Accounting, Tax

Andreas is an International Tax Manager at Schlecht & Partner in Stuttgart, Germany. Specialising in transfer pricing and international tax advisory, he worked at a Big4 firm in Germany and Canada as well as for multinational automotive firms in international tax. Contact Andreas.